A discount rate, or discount ‘factor’, is calculated and applied to each year’s cash flow, in order to arrive at the present value. DCF shouldn’t necessarily be relied on exclusively even if solid estimates can be made. Companies and investors should consider other, known factors as well when sizing up an investment opportunity. In addition, comparable company analysis and precedent transactions are two other, common valuation methods that might be used. Discounted cash flow analysis can provide investors and companies with a reasonable projection of whether a proposed investment is worthwhile. Adding up all of the discounted cash flows results in a value of $13,306,727.

Why is a Terminal Value Used

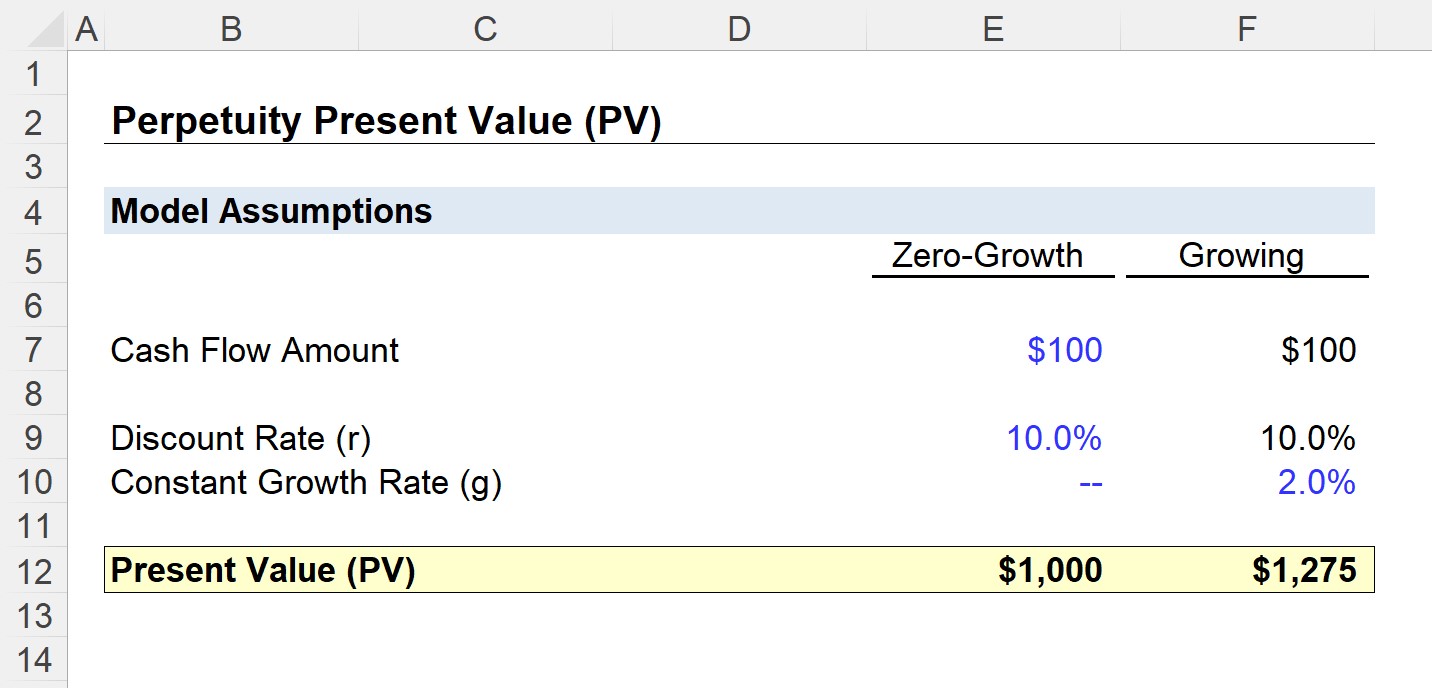

The net present value of a perpetuity is not as large as it might seem because the time value of money erodes the value of dollars far into the future, due to inflation. Therefore, the cash flows received by a fixed perpetuity many years from now can become negligible in terms of future buying power. In finance, perpetuity is defined as a continuous stream of identical cash flows with no end. The concept of perpetuity is used in several financial theories, such as in the dividend discount model (DDM).

Example from a Financial Model

Typically, perpetuity growth rates range between the historical inflation rate of 2 – 3% and the historical GDP growth rate of 4 – 5%. If the perpetuity growth rate exceeds 5%, it is basically assumed that the company’s expected growth will outpace the economy’s growth forever. The discounted cash flow (DCF) model is probably the most versatile technique in the world of valuation. It can be used to value almost anything, from business value to real estate and financial instruments etc., as long as you know what the expected future cash flows are. The exit multiple model for calculating terminal value of a company’s cash flows estimates cash flows by using a multiple of earnings.

How to Calculate Terminal Value: Discounting Terminal Value and Calculating the Implied Share Price

Discounted cash flow and net present value are not the same, though the two are closely related. After forecasting the expected cash flows, selecting a discount rate, discounting those cash flows, and totaling them, NPV then deducts the upfront cost of the investment from the DCF. For instance, if the cost of purchasing the investment in our above example were dcf perpetuity formula $200, then the NPV of that investment would be $248.68 minus $200, or $48.68. Two, select a discount rate, typically based on the cost of financing the investment or the opportunity cost presented by alternative investments. Three, discount the forecasted cash flows back to the present day, using a financial calculator, a spreadsheet, or a manual calculation.

The DCF Model: The Complete Guide… to a Historical Relic?

- The forecast period is typically 3-5 years for a normal business (but can be much longer in some types of businesses, such as oil and gas or mining) because this is a reasonable amount of time to make detailed assumptions.

- Calculating FCFE would require you to project the financing cash flow (like borrowings, repayment and interest).

- He is an expert on personal finance, corporate finance and real estate and has assisted thousands of clients in meeting their financial goals over his career.

- In order to calculate Free Cash Flow projections, you must first collect historical financial results.

Depreciation is a non-Cash expense, meaning the company books Depreciation as an expense on the income statement for GAAP (Generally Accepted Accounting Principles) purposes but in reality, no Cash was actually spent. Therefore, in order to calculate true “Cash flow,” this must be added this back. Similarly, CapEx must be subtracted out, because it does not appear in the Income Statement, but it is an actual Cash expense. The assumptions driving these projections are critical to the credibility of the output.

DCF Terminal Value Excel Template

Also, macroeconomic conditions affecting the business and the country may change structurally. It isn’t easy to project the company’s financial statements showing how they would develop over a longer period. Let’s take a company that has two shareholders owning 70% and30% each. If the company’s equity value is $10,000,000, a buyer looking toacquire the 30% position would not pay $3,000,000 because of the lack ofcontrol attached to this minority shareholding.

If the discounted cash flow is higher than the current cost of the investment, the investment opportunity could be worthwhile. The Risk-Free Rate (RFR) is what you might earn on “safe” government bonds in the same currency as the company’s cash flows (so, U.S. Treasuries here). You value the company in both these periods and then add the results to get its total value from today into “infinity” (AKA until the Present Value of its cash flows falls to near-0). Theoretically, this can happen when the Terminal value is calculated using the perpetuity growth method. This is because we have normalized (stabilized) the terminal year projection. Think about this, when a business is growing at double digits, usually they are pouring a lot more resources to support the growth.

It is an analysis that can be applied to a variety of investments and capital projects where future cash flows can be reasonably estimated. Dividend discount models, such as the Gordon Growth Model (GGM) for valuing stocks, are other analysis examples that use discounted cash flows. Discounted cash flow analysis is used to estimate the money an investor might receive from an investment, adjusted for the time value of money. The time value of money assumes that a dollar that you have today is worth more than a dollar that you receive tomorrow because it can be invested.